Equity Vs Peer-to-Peer: Which Works for You?

Crowdfunding can generally be broken down into two categories; equity based investing and peer-to-peer (P2P) lending. Both methods of funding are effective however and they have been responsible for funding many thousands of Start-ups. For many business owners looking for financing, crowdfunding platforms have become the first choice over the banks.

It’s true to say that P2P platforms are more popular amongst investors, and this segment has a global funding volume of more than US$25b – 10 times that of equity based platforms. Whilst the majority of the funds raised are still invested in Start-ups, both are growing exponentially in the property sector.

So, how does Equity Crowdfunding match up?

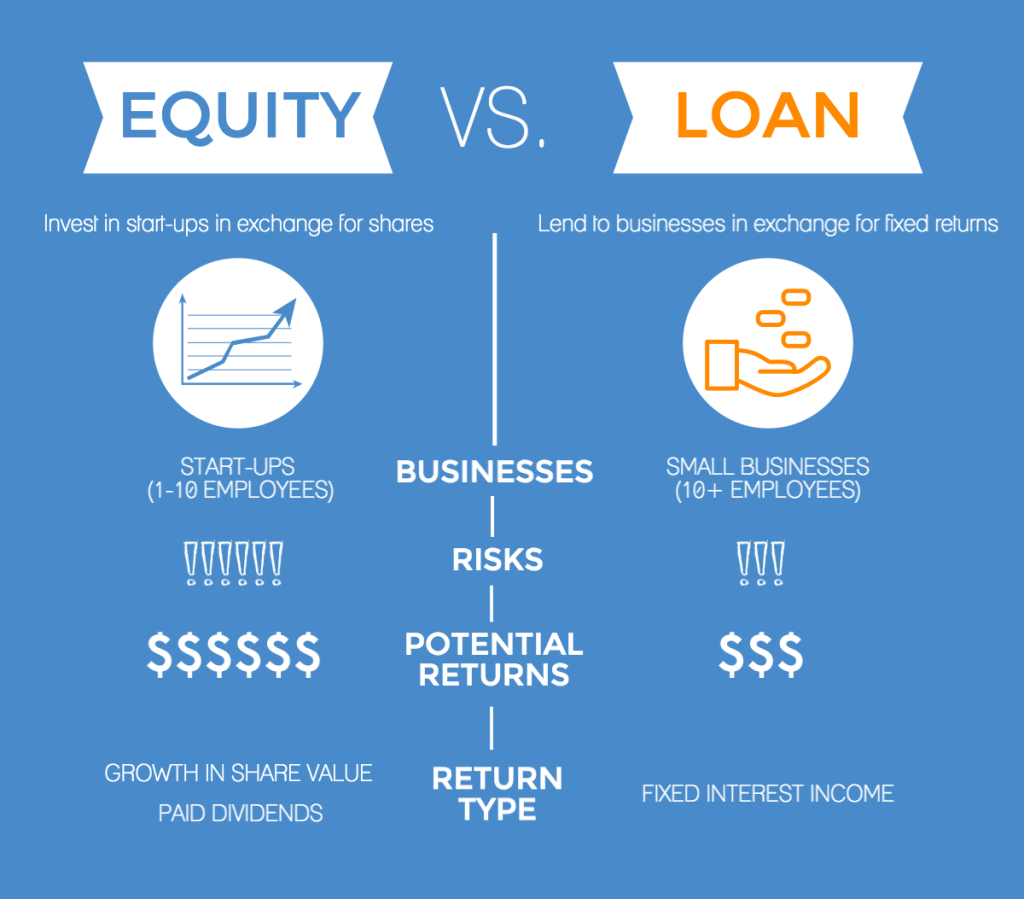

The image below (courtesy of symbid.com) sums up the main differences between equity investing and P2P lending.

Although there are many technical differences between the two, there are three main areas which are the big deciding factors for investors:

- Risk

- Return

- Return Type

Risk

It is important to remember that all investments carry risks, no matter what people say. P2P platforms, tend to offer lower risk, due to several factors such as shorter investment terms, borrowers with a good credit rating, lending limits similar to those offered by the banks. They also have lower entry levels for each investment making it easier to spread your risk across a number of borrowers.

We understand that investors accept risks as long as they know what they are. So we include our own risk rating system that looks at different aspect of our investments and scores each one so that they are easier to compare. Click here to know more about our Risk Return Profile.

The golden rule of investing is to spread your risks, and by investing through CrowdLords, you get the chance to not only invest in BTLs, but other also in other types of property investment including refurbishments, conversions, new developments and soon commercial property as well.

Return

The Return is arguably the most important aspect for investors. P2P platforms provide a very good return – at least 2 or 3 times the interest rates currently offered by the banks. Given that the risks associated with P2P investments are relatively low, it is no surprise that the levels of return tend to be low as well.

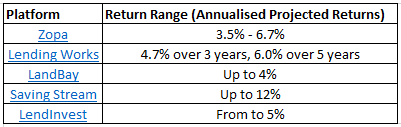

The table below shows the top 5 (in no particular order) P2P lending platforms and their return range, assuming you take part in a 12 month investment.

These returns are often considered low compared to the returns offered on equity based crowdfunding platforms like CrowdLords, where projected total returns are usually between 9% and 25% p.a.

Return Type

The type of return produced by equity and P2P investments are also very different.

As suggested, equity based platforms turn property investors into property shareholders, and with the help of an SPV, the property is administered like a company would be, distributing income as dividends to the investors in return for their funds. Whereas P2P investments pay the returns in the form of interest, just like a bank would.

P2P returns are also fixed, which means if the property gets sold at the end of the term, the investor is not able to take advantage of any capital gains. For the serious property investor, who expects to benefit from the growth in value of the property over time, equity crowdfunding as much more to offer.

As a property investor, it is important to spread your risks, and if you’re already an active P2P investor, and want to give equity crowdfunding a go, then you simply need to register and click the Browse Investments button.

- Is post-war property a good investment?

- Can post-coronavirus unused office space resolve a nation's housing crisis?

- Are you an optimist or a pessimist in Property Crowdfunding?

- Need a hand with puzzling alternative finance jargon?

- Seven myths and one truth about Property Crowdfunding

- Understanding Loan to Value (LTV) - Part II

- Understanding Loan to Value (LTV) - Part I

- Construction workers given the green light to work despite the Coronavirus pandemic

- Is Coronavirus likely to slow down growth in the UK's property market?

- How the decline of UK's High Streets is opening the way for UK property developers

- Who should you turn to for investment advice before Property Crowdfunding?

- Is property crowdfunding a viable way to get onto the property ladder these days?

- The importance of liquidity in your investment portfolio

- FCA guidance changes ring in the new year

- Gender stereotypes in Alternative Finance; are women playing catch-up?

- How does CrowdLords compare?

- Brighton Road - Meet the Developer

- Property Crowdfunding; A Global Appeal for UK Platforms?

- Does the future of Property Crowdfunding lie in the hands of Millennials?

- Meet the Developer - Jo Hagan (5 Mentmore Terrace)