Understanding the capital stack with different levels of investing

In a nutshell

When entering the world of Alternative Finance, one of the most important things to consider when lending capital against an asset, or investing funds into a project, is the security of your money in comparison to the projected returns.

Not only should you carry out a series of personal due diligence processes in order to determine whether the type of property investment is right for your financial circumstances, but you should also analyse the specific type of property investment you want to make, depending on the level of risk you are willing to accept, as well as the projected returns you hope to receive.

Therefore, the Capital Stack is a useful financial topic to learn about, as it simplifies the numerous categories of property investment types available, each corresponding to the level of risk involved, in a user-friendly, easy to decipher way.

What different types of assets are there in investing?

When investing, certain assets are considered to be fairly dependable as they are either usually in demand, like property, or they are easy to sell and convert to cash in a relatively short space of time. Assets not immediately quick and easy to sell, like property, are called "illiquid assets". Assets that are relatively easy to convert to cash quite quickly are known as "liquid assets". Liquid assets include items like jewellery, gold, luxury watches, classic cars or fine art. The security on these assets provides a legally binding assurance that in the event of a default on the loan contract, they would be sold to repay the investors.

However, for newcomers to the world of Alternative Finance, the word "security" can be misleading to inexperienced property investors as it may imply a safety-net which guards against the risks involved. This is where the idea of the "Capital Stack" can be introduced, but it requires some explanation.

What is the Capital Stack?

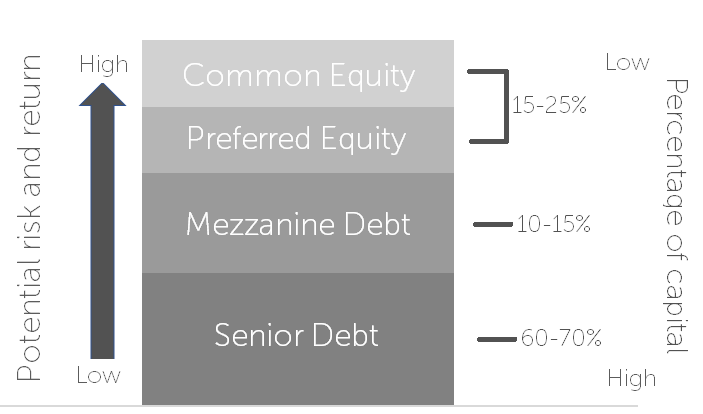

In short, the Capital Stack is best described graphically as a "tower" detailing the specific tiers of investment into which you can invest. These tiers portray the different levels of risk involved as a direct consequence to the subsequent level of potential returns gained. It is a hierarchy of creditors listed in ascending order under the hypothetical, but very possible situation of a loan defaulting.

In theory, while there is no limit to the number of layers the Capital Stack may contain, we can normally divide it into these four main categories;

- Common Equity

- Preferred Equity

- Mezzanine Debt

- Senior Debt

The most important points to remember to understand how the Capital Stack works are that each level has seniority over all the capital sources located above it in the stack. Conversely, each capital source is subordinate to all the other levels located below it.

*The above infographic is being provided by CrowdLords for illustrative purposes, only based on CrowdLords's analysis and understanding of the Capital Stack.

What does Senior Debt involve?

Let's look at the base of the graphic as an example. Should you choose to invest via the Senior Debt, you are choosing the least risky option as Senior Debt is usually secured with a 1st charge. Therefore, in case of the loan defaulting, although you hold precedence over the other levels when recovering payments, you will always receive the lowest returns.

How is Mezzanine Debt different?

Likewise, as Mezzanine Debt is positioned above Senior Debt in the stack, should the loan default, if you choose to invest via this method, you will only receive your repayments once all the Senior Debt obligations have been met. As Mezzanine Debt is usually secured with a 2nd charge and is therefore slightly riskier than Senior Debt, logically, the projected returns are somewhat higher.

You should try to bear in mind that should a loan default, if there are insufficient funds to fully repay all the capital, as the risk increases the higher up the stack you move, then losses are incurred from the top down. As a result of this, projected returns on investments will increase the higher up the stack you invest.

Preferred Equity

Having covered the lower "debt" levels of the Capital Stack, this brings us to the upper "equity" investment layers. As we have established, risk is significantly higher as equity holders are the owners of stocks and shares in the Special Purpose Vehicle (SPV), set up by the borrower. In addition, unlike with debt investors (Senior and Mezzanine) who are usually paid a fixed interest rate, returns to equity investors come from the profit generated by the SPV. Because of this, you will only be repaid after the company has met its obligations to its lenders.

Equity investments can offer the investors higher projected returns because of the risk involved, but this is deemed to be worthwhile by many property investors as the returns specifically depend on the profits made by the company. Sometimes returns will be more than initially projected and sometimes they will be less, appealing to those property investors with a bigger appetite for risk.

Common Equity

As seniority on the Capital Stack flows in ascending order, Preferred Equity investors are above Common Equity investors in order of priority. As a result, although holding a Common Equity investment is the riskiest form of investment on the stack, at the same time it can also be the most lucrative. As we've established, in the event of indebtedness, every other category on the stack will get fully repaid before Common Equity holders (providing there are sufficient funds to do so). Nonetheless, the benefit is that if the project being funded, or the business is successful, Common Equity investors can potentially enjoy the most lucrative returns.

Choosing your position on the Capital Stack

It is important to establish that there is no right or wrong position to hold on the Capital Stack, only different levels of investments that different types of property investors will find appealing based on personal financial circumstances and appetite for risk.

We would recommend property investors to have a diversified portfolio as this can reduce overall risk exposure while maintaining long-term appreciation. You can do this by spreading different investments up and down the Capital Stack in the form of investing in numerous projects.

By understanding the Capital Stack, you can become empowered to make more informed decisions as to where in the Alternative Finance market you feel comfortable with your own investments, as well as whether the risks you are willing to take correspond adequately to your expected rewards.

- Is post-war property a good investment?

- Can post-coronavirus unused office space resolve a nation's housing crisis?

- Are you an optimist or a pessimist in Property Crowdfunding?

- Need a hand with puzzling alternative finance jargon?

- Seven myths and one truth about Property Crowdfunding

- Understanding Loan to Value (LTV) - Part II

- Understanding Loan to Value (LTV) - Part I

- Construction workers given the green light to work despite the Coronavirus pandemic

- Is Coronavirus likely to slow down growth in the UK's property market?

- How the decline of UK's High Streets is opening the way for UK property developers

- Who should you turn to for investment advice before Property Crowdfunding?

- Is property crowdfunding a viable way to get onto the property ladder these days?

- The importance of liquidity in your investment portfolio

- FCA guidance changes ring in the new year

- Gender stereotypes in Alternative Finance; are women playing catch-up?

- How does CrowdLords compare?

- Brighton Road - Meet the Developer

- Property Crowdfunding; A Global Appeal for UK Platforms?

- Does the future of Property Crowdfunding lie in the hands of Millennials?

- Meet the Developer - Jo Hagan (5 Mentmore Terrace)